2nd Chance is one of those stocks I used to own in the past because of the steady dividends they pay but have since divested them at around $0.455. They have given me quite a good appreciation and dividends over the past couple of years, so I must say it's definitely good investment return for me.

Over the past few weeks, the share price has been trending down fiercely and today it makes its way down to a low of $0.38, pretty fierce if you ask me. Now, the big question is if the current price of $0.38 justifies an opportunity to buy?

I am probably not going to run through all the details about the company but just wanted to highlight on a few things to note:

1.) Failed execution of spinning properties into Reits

This is probably the biggest reason why the share price have plummeted downwards fiercely.

When news first broke out that they were going to spin off their properties into a Reit and a potential special dividend might be issued, investors were jumping to joy and these has sent their share price rocketted upwards.

On the eve of the New Year, the company has confirmed that SGX has rejected their letter of eligibility to list the Fund by the Target Date. The proposed spinoff has now collapsed. What I have read from The Edge magazine was that SGX seems reluctant to allow the proposal to go through as they were holding strata type of the building rather than the whole building itself, which is what most Reits have.

This has major repercussions as we will probably see in the later parts.

2.) IAS 40 - Fair Value Accounting

I've mentioned this new reporting standard a couple of times in my previous articles so I will not be repeating them again.

As you can see from the above failed spin-off, it means that the company is unable to divest their properties at a good timing and a good price and are now having "stuck" to hold huge amount of property assets in their balance sheet. One negative impact I can think of immediately was capital is locked and they are unable to be recycled, mostly to repay borrowings cycle they are currently engaged in.

What IAS 40 makes it worse is that the company has been recognizing fair value gain over the past few years because of the appreciating asset which boosted the equity portion of the earnings. Now that the properties cycle is on the other end, the company would most likely having to recognize a fair value loss, which was what happened in the recent Q1FY15 they had reported. This will have a downside pressure on earnings and book value as the equity portion will keep decreasing if this goes on.

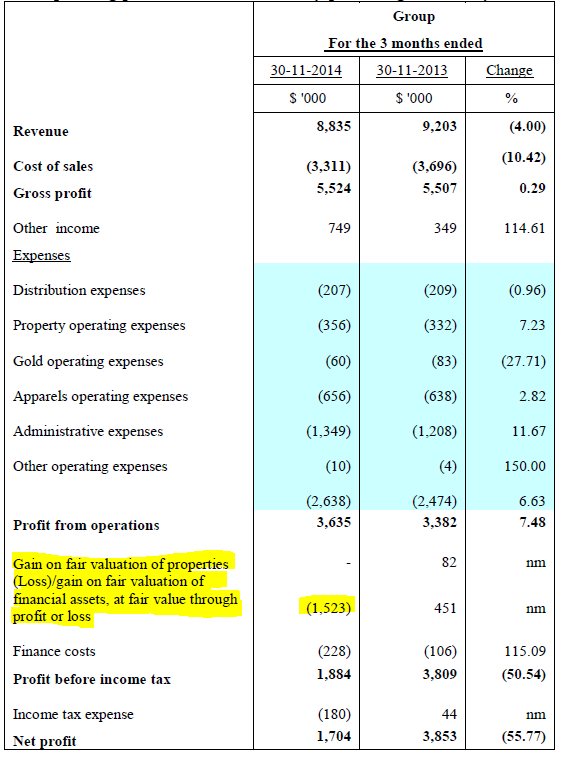

|

| Q1 FY15 Results |

3.) Core business activities facing pressure and competition

This leads us to the next point.

If we deep dive down into its core business activities, we see that their earnings are mostly concentrated from their properties activities, including recognizing the fair value gain on their investment properties. This can be pretty risky if the sector is in a decline like it is right now.

|

| Revenue Q1 FY15 |

|

| Profit Q1 FY15 |

Apparel business is facing some negative profitability due to the closure of some shops and competition wars while the gold business margin is dropping due to the falling retail price. It is quite obvious that the core activities are facing some headwinds heading into the future, which will bring downward pressure on earnings.

4.) Outstanding New Warrants

This is a tricky one to be honest.

The new warrants are currently issued at $0.40 and are exercisable during 25 July 2016 to 24 July 2017. The number of outstanding new warrants for this is huge at 577,024,950.

The immediate reaction to this will always be dilution for the existing shareholders, at least for the period mentioned above. Still, the current market price is at $0.38 at the moment so as it seems dilution will not take effect unless it goes above $0.40 otherwise.

The interesting thing about them issuing warrants is that the management is confident that the conversion will take place and they will use this proceeds to repay off the borrowings. This is what they did back in 2012 when the warrants converted amounted to $25.31 million and they used this to repay off their borrowings. In my mind, the cycle goes like this:

Borrow money --> Issue high dividend --> Push up share price --> Issue warrants --> Conversion used to repay borrowings

It appears that if none of these warrants are exercised by the above period, then the company will have to think of alternatives to repay its borrowings, which is mostly short term.

We can see why existing investors are concerned about the dilution which may take place by then. If assuming all the warrants are converted, this will add into the outstanding shares to become 677,210,218 + 577,024,950 = 1,254,235,168. What this means is if the EPS annualized is $0.01 currently, you will get $0.0054, which is almost 46% diluted. Last year dividends alone amounted to about $0.037 cents/share. This is a huge concern if you ask me.

Conclusion

Mr. Salleh is a good businessman with a very candid profile who are very honest about his business.

The whole objective is to ultimately turn the business into a billion dollar market cap project with the process of driving up earnings through proper recycling of its assets, enticing investors into the high dividends it pay out (sometimes even through borrowings), issuing the warrants, pushing up the share price, using the conversion to repay off the borrowings and repeating the cycle.

Using a quick reverse valuation model, I assume the current price at $0.38, last year earnings per share at $0.0244 (stemming out any one-off gain), a discount rate of 15%, and I get a perpetuity growth of 8.7%. If you are in any doubt, just ask yourself whether the terminal growth rate of 8.7% is sustainable to warrant a current price of $0.38. This is assuming undiluted. If there are dilution involved in a later stage, the perpetuity growth will increase to 11.5%.

Maybe you will get an answer and give yourself that second chance to decide.